For most homeowners, I think it is going to be difficult to let go of the last few years.

- ‘Our house appreciated $75,000 in 5 years!’

- ‘Really? Our house went from $300,000 to 400,000 in 4 years!’

- ‘Not bad, but ours went from $150,000 to $400,000 in 3 years!’

Unfortunately, we won’t be saying that as often as we used to anymore.

A Return to Normal Appreciation

Being a homeowner, especially a first-time homeowner, has been a lot of fun for the past 5 years. The rate of appreciation has been substantial for most everyone in the post-bubble market. No matter where you live or what you bought, if you signed the closing statement in 2012, you are up anywhere from 20 to 40% in the years since.

But as we approach the end of 2018, we can expect to see future appreciation rates on housing return to the norms of the 1990’s and early 2000’s. And for those who know nothing about the good old days, I am talking about 2 to 4% in any given year (and yes, I realize how boring that sounds.)

That said, imagine if all of this topsy-turvey upsidedown-ness hadn’t happened, or even if prices had fallen over the last five years. Would you have been better off if you hadn’t bought at all?

The answer is simply –– nope.

Why? Because renters always lose in the long run.

Boiling a Frog

There is an old adage about boiling a frog (and no, I have not done this before so don’t call PETA). But it goes like this: If you put a frog in a pot of boiling water, it will immediately hop out. But if you put a frog in a pot of cool water and then put it on the stove, the temperature change is so gradual that the frog will stay in until it is too late.

And for this reason, frogs rent.

If you’re a renter feeling upset because I just compared you to a frog, don’t. For many, renting does make sense. Temporary situations, an uncertain future, recovery from a financial catastrophe, etc –– these reasons all make sense.

But if you are going to be here for a while, are trying to make a smart investment, or are otherwise in a position where you could own but don’t, then you are exhibiting frog-esque characteristics.

Tracking Rents

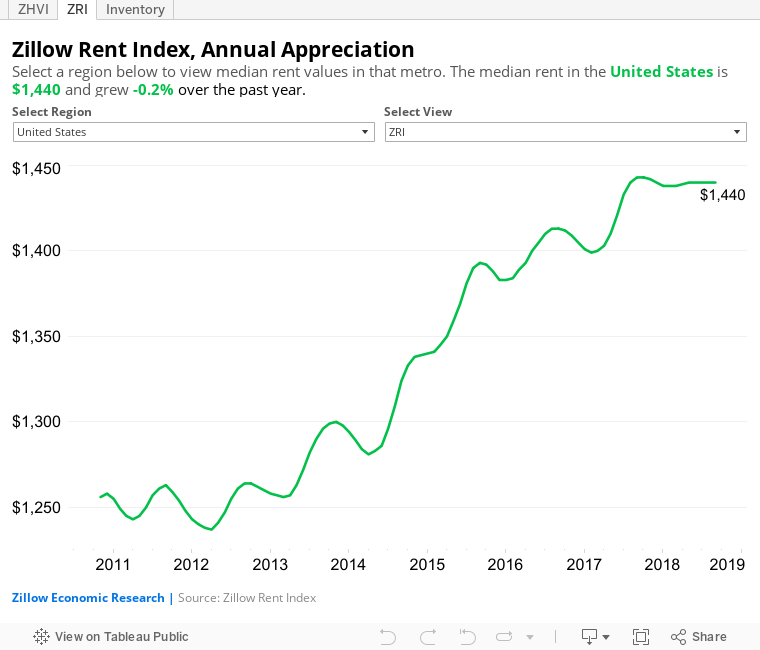

Zillow, for all of its warts (see what I did there?), has managed to aggregate a lot of really good data and they make it available if you know where to look. And besides tracking housing values (for which they are primarily known), they also track rents.

Take a look at this (use the drop down menu to find RVA, or to look at other markets):

Since 2011, rents in Richmond VA have gone up from an average of $1,179 per month to $1,391 per month. That’s nearly an 18% increase if you are scoring at home. And that chart is for the Richmond region as a whole. Areas such as Shockoe, Manchester, and Scott’s Addition are up by a much larger percentage.

Now, let’s think about the other side of the equation. Do you know how much of your mortgage you would have paid off in the same time period? If you had a 30-year mortgage at 4.5%, you would have paid off anywhere from 10 to 12% of your mortgage in the same time frame.

So even if your home had not grown in value by a single percentage point, owning would mean your payment would have remained the same, your debt would be 10 to 12% lower, and you would have also picked up a nice little tax write-off for the interest you had paid (but please consult your tax advisor to find out how much the Mortgage Interest Deduction would have saved you.)

It doesn’t take a math major to figure out that a fixed payment, lower debt, a nifty tax break, and the potential to eventually not have a house payment once your mortgage is paid off are all pretty good things.

Ribbit.

Elective Renting is a Poor Strategy

The housing market is rapidly putting the finishing touches on its post-bubble recovery and is approaching a time where housing appreciation will revert to the more normal rates of the 1990’s and early 2000’s. The promise of steep appreciation will not be what makes housing the sole reason for ownership as we move into the next decade.

Instead, the reason that housing will be one of the best assets you can own will be related to the reason it has always been a great asset –– its long-term value as a part of your portfolio will dwarf the short-term savings associated with renting.

So don’t fall for the ‘well, I should have bought 5 years ago so I should wait for the next bubble to pop’ logic. You will be far worse off.

Don’t believe me? Ask your landlord.

Getting Out of the Pot in 2019

So as 2018 comes to a close, be thinking about the fact that you will soon be getting a note from your management company notifying you of your new water temperature … errrr … rental rate for the coming year. If the landlord does their job right, the increase won’t make you leave –– it will be just enough to make you grumble, but stay.

So as 2018 comes to a close, be thinking about the fact that you will soon be getting a note from your management company notifying you of your new water temperature … errrr … rental rate for the coming year. If the landlord does their job right, the increase won’t make you leave –– it will be just enough to make you grumble, but stay.

Interest rates are beginning to edge up after years of staying below trend and house prices are still creeping upwards, too, albeit at a slower pace. Waiting for prices and rates to drop to 2012 levels again is simply not a winning strategy.

Is it getting a bit warm in here? Or is it just me …