Agent: Congratulations! You are under contract!

Client: Great! So we are done, right?

Agent: Not exactly. Anywhere from 10% to as high as 20% of contracts fall apart for one reason or another.

Client: Wait, what?!? There is as much as a 20% chance that the contract I have on (or for) my house will fall apart?!? How can I make any plans going forward with that much uncertainty?!?

Agent: Let’s talk about why.

The Back on Market Statistic in MLS

First, let’s talk about where we get the data.

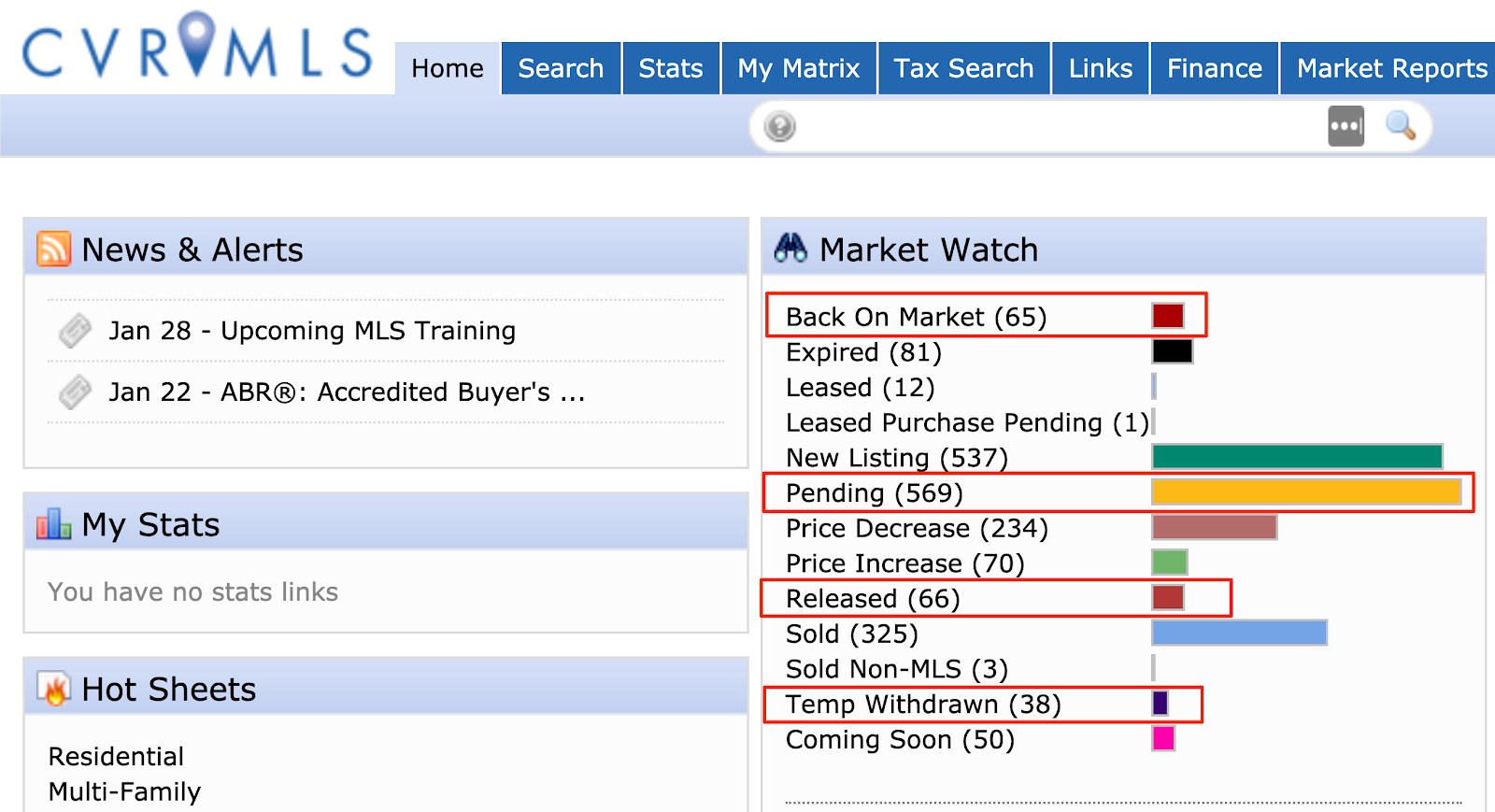

The Multiple Listing Service tracks a lot of statistics –– one of which is called ‘BACK ON MARKET’ (or BOM).

BOM measures the number of homes whose status changes from ‘PENDING’ (meaning under contract) back to ‘ACTIVE’ (meaning ‘available for sale.’)

Computing the Failure Rate

A random sample of a week in middle January yielded the following results:

- 569 homes went PENDING

- 65 came BACK ON MARKET

- 65/569 = 11.4% contract failure rate

(A quick note –– a week later, the number of ’Back On Market’ properties, jumped to nearly 14% with 40 of 295 coming back to Active status from Pending –– so this metric will change week to week.)

Released and Temporarily Withdrawn

Now if you note the screenshot, you will see where RELEASED and TEMP(orarily) WITHDRAWN are also highlighted:

- RELEASED –– meaning that the listing agent and owner have agreed to part ways.

- TEMP WITHDRAWN –– meaning probably what you think, the home has been removed from the market for an unspecified period of time per the seller’s request.

Both of these status changes (66 Released + 38 Temp Withdrawn = 104) often come on the heels of a failed contract –– and thus the count of the Back on Market is most likely higher.

Between 10% and 20%

So, yes, somewhere between 10% and 20% is the correct number.

This number will vary based on what time of year you examine, what price point you are in, and what geography you study and of course, what percentage of the Released and Temp Withdrawn homes you assume were the result of a failed contract.

Why Don’t Homes Close?

A 10% fallout rate is a big number. A 20% fallout rate is even bigger.

When you are making irrevocable (and expensive) commitments that depend on a successful settlement, 80% certainty doesn’t feel great, does it?

It shouldn’t.

Let’s discuss the reasons.

The Primary Reasons

Homes don’t go to settlement for any variety of reasons –– but they generally fall into one of the following categories:

- Lender incompetence

- Appraisal less than the sales price

- Inspection issue

- Agent incompetence

- Cold feet

Let’s discuss each.

Lender Incompetence

I cannot stress this enough –– work with a lender with the following characteristics:

- They are local (not Quicken, USAA, or some other internet lender)

- They are tied to a bank (meaning they have ‘shelf loans’ or other specialty products)

- They do a lot of business with the agent (you will be on the top of the pile and receive favorable treatment when positive underwriting interpretations are required)

- They have a full range of products (many lenders only have a limited product menu and will try to place you in the wrong product because they don’t have the correct option)

- They have a ‘Lock and Drop’ feature (meaning that if rates drop during the lock period, you receive the lower rate)

- They are not your Credit Union (contrary to common belief, CU’s do NOT give better rates and their representatives are typically not licensed)

Furthermore, when it comes to niche purchases (condos, rehabs, multi-family) or complex underwriting (divorce, business owner, commission income) using a mortgage company with specialists in the specific loan type is critical.

Alas, few borrowers (or agents) know how to find those who specialize in the specific niche required.

The Dreaded Internet Lender

To the Sellers –– if you are a seller and you receive a contract from a purchaser who plans to use an internet/non-local lender, accept the contract at your own risk and do not be surprised when, at the 11th hour, you get the dreaded ‘we have a problem’ message.

To the Buyers –– if you are a buyer and in a multi-offer scenario, using Quicken (or USAA) is an almost near guarantee that you will not be the winning bid. Why? Because listing agents know how difficult and unreliable internet lenders are.

Internet lenders can be decent for refinancing (mostly because a missed closing date isn’t overly penal,) but for purchasing a home, they just carry too much risk.

Cheaper Isn’t Better, It Isn’t Anything

A rate that is ½ point lower that closes late (or not at all), is not a better rate –– it is actually more expensive!

Late closings trigger penalties, loss of deposits, and a handful of other emergency decisions (hotel stays, storage units) that eat up any savings that the rate promised.

The bottom line is that the local lender puts their reputation and well-being on the line every time they issue a pre-qualification letter. If their organization can’t perform as promised, they don’t just lose the current deal, they lose the rest of them.

An Appraisal Issue

When prices are accelerating rapidly (especially in the spring), comparable sales lag where the market is.

In other words, when you are trying to establish the fair market value of a home in March of 2020 –– and the sales comps are from the fall of 2019 –– you will not find the sales from yesterday you need to justify the price today.

But unfortunately, that is how the appraised value is determined –– via PAST sales.

We like to say that using comparable PAST sales to establish value TODAY is like driving while looking out of the rearview mirror –– it tells you where you were, but not where you are going.

When you, as a seller, have accepted a contract on a home where there were multiple bids, odds are, the sales price has been pushed above the value at which the home will appraise. When a loan is subject to appraisal (as many loans are), an appraisal below the sales price places the loan in jeopardy.

Appraisal Math

Applying some numbers –– if the purchaser is putting 10% down on a $300,000 sales price and the appraisal comes in at $290,000, the seller is responsible to make up the difference –– in other words, they have to find an additional $10,000 in down payment.

If the purchaser has no excess cash (or is unwilling to access it), then the seller is forced to either:

- lower the price to the appraised amount

- accept the loan denial and put their home back on the market

The bottom line is, as a seller, you have to look at the type of financing the purchaser is using –– and specifically how the appraisal contingency is worded –– to properly judge how susceptible you are to the appraisal causing the contract to not move forward.

A good agent knows how to assess the risk.

Inspection Issues

Inspections are the bane of almost every agent’s existence.

Essentially, you have buyers who feel like they overpaid (and feel entitled to a perfect home,) sellers who see every issue as cosmetic, and inspectors who feel it necessary to point out every flaw, including that the doorbell is not at the correct height (not kidding.)

On the other end of the inspection report are agents who know very little about construction and contractors who both disagree with the inspector’s assessments and cost estimates, and are trying to generate even more business for themselves by spooking the clients –– all trying to decide if a $100 piece of siding is rotten or just soft.

It is maddening.

Call it pride, call it short-sightedness, or simply stupidity, but way too often we see $500 worth of inspection items torpedo $300,000+ sales

($500 / $300,000 = .0016, in case you wanted to see how inconsequential that amount actually is.)

No Home is Perfect

At the end of the day, as a buyer, be prepared to take the home with a few issues –– especially given the market conditions. Are we saying that a cracked foundation, a failing 50 year old roof, and radon readings in the 100’s are not issues? Of course not. But when minor carpentry issues, a few questionable double taps on your main circuit panel, and wobbly toilet are found, it is ok. Don’t freak out.

And a final note for sellers –– I have yet to see a house that comes back on the market get a better offer. Digging in to save yourself $1,000 only to cause your buyer to flee is a poor strategy. You are almost always better off to work with the offer in hand, even if it means swallowing your pride and working out a deal that feels one-sided.

Agent Incompetence

My first broker was fond of saying that, as an agent, when you have a willing buyer and a willing seller, get out of the way.

It is one of the truest statements he ever uttered.

Far too often, in an effort to either feed an ego or justify the commission, agents will engage in activities that complicate or sabotage the transaction. Speaking too much, introducing doubt, blaming the other side, making mountains out of molehills –– all of these actions put unnecessary pressure on a transaction when there needn’t be.

The net result is it exhausts everyone’s emotional energy to such a point that the sides oftentimes become unable to work through an issue that normally would not derail the transaction.

It happens far more than it should.

Cold Feet

And yes, every once in a while, a simple case of cold feet (i.e. –– Buyer’s Remorse) is the culprit.

Typically, buyer’s remorse occurs when a) the deal is too one-sided, or b) the purchaser didn’t fully do their homework before finding themselves under contract to purchase a home.

Agents and Uncertainty

As an agent, it is absolutely your responsibility to make sure the buyer understands their decision:

- Educated and confident buyers make decisions that stick

- Buyers who never developed a true understanding of market conditions tend to walk away

Agents –– if you want your deals to stay together, empower and involve your clients.

Summary

So yes, not all deals go to settlement.

Statistically speaking, somewhere between 10% and 20% will fall apart for one reason or another. And thus, some percentage of sellers will have to go ‘Back on the Market’ after experiencing the frustration of a contract that did not stick.

So, as a seller, how in the world do you defend against being left at the altar?

Well, that is Part II of the series …