The phone rings –– you don’t recognize the number, so you answer.

On the other line is a Realtor, who says that they have a buyer who is interested in buying your property, and that they have a written offer in their hand. Would you consider selling it?

Well, you know that the market is good and that prices have gone up, so you engage.

‘How much?’ you ask.

The Realtor on the other end of the phone tells you a number that is way above what you ever dreamed your home could fetch –– AND you wouldn’t have to pay a listing fee.

You do some quick math –– sales price, back out a small commission for the agent, subtract what you owe –– and try to contain your excitement.

You hadn’t planned on selling, but that is a pretty big number.

You say, ‘Send it to me …’

The Money You Missed

A large chunk of money is hard to resist when offered –– especially when you aren’t expecting it –– and it can catch you off guard.

But do you know what is better than a high sales price? A HIGHER sales price with better terms.

‘And how exactly do you propose that one turns a large payoff to an even larger one?’ you might ask.

Easy, you leverage the greatest invention in the history of mankind when it comes to housing –– the Realtor Multiple Listing Service (MLS.)

How to Harness the Power of MLS

So how exactly does MLS create value for the seller?

Simple –– it harnesses the power of the network and amplifies it to your benefit.

MLS tracks somewhere between 95% and 99% of all real estate transactions –– meaning that anyone who is serious about purchasing a home uses it as their primary mode of finding a home.

Yeah, I get it. Zillow, Trulia, Realtor.com have the same info and better user interfaces yadda yadda yadda, but guess where Zillow et al get their information? You guessed it, MLS.

So when you offer your home for sale and put it into MLS, you immediately broadcast its availability to a network of 6,000+ Realtors working with 95%+ of the buyers in your market (as well as ZIllow, Trulia, and Realtor.com, too.)

The impact is nearly instantaneous –– everyone who needs a home comes rushing all at once to try to buy yours.

Creating an Auction is Simple (if you know how)

If you have ever been to an auction, you’ve seen the impact.

If you only have one person who wants the item up for bid (which is rare), well it typically doesn’t get top dollar.

However, all it takes is two people vying for it –– and the price escalates quickly.

If you have three or more, you can guarantee the price will escalate well in excess of the item’s value –– and thus, the goal for any auctioneer is to tempt three or more people into a simultaneous bidding war.

That is why sellers love (and buyers hate) auctions. Multiple buyers keep one another honest and force everyone to dig deep and pay up.

Auctions identify the most desperate buyer and make that individual defeat everyone else to win the prize. And when there are hordes who all want the same thing, prices and terms reflect the fact that demand is well in excess of the supply.

And I have some good news –– good Realtors know to leverage MLS to create auction-like conditions. So if you know how to make MLS function as a de facto auction, you can create the most value imaginable for your selling clients.

Unless, of course, someone sells their home without using MLS.

The Impact of Buyer Competition

When you bid at an auction for a piece of art, or maybe some other rare artifact, generally the price that is paid is the only thing that matters.

When you sell real estate, price obviously matters, but so does the structure of the financing, amounts of the deposits, the terms of the inspections, the terms of the appraisal, any rent backs or other extended possession agreements, closing dates, personal property, etc. –– all of which create seller value over and above the price.

So, while the competition will drive the price up, a shrewd seller (or more specifically, their agent) will leverage the competitive environment to simultaneously shift the remainder of the contract’s terms in favor of the seller.

Examples

An offer that is bid up to say, 10% over the asking price, but with an appraisal contingency that could bring the price back down if the appraisal is less than sales price, then the seller is at risk for the price to be reduced in the event of a low appraisal (happens all the time, by the way.)

An appraisal contingency is a contractual right the purchaser wants to maintain in any offer. However, if a competitive offer waives the appraisal contingency, it forces everyone’s hand and you typically see other offers follow suit.

Similarly, if the purchaser offers a $10,000 deposit that returns to the purchaser in the event that their loan is denied, but someone else makes the deposit non-refundable, well the seller is in a far stronger position to leverage both offers to make the deposit non-refundable.

When the seller has leverage, nearly all risk in the contract can be shifted from the seller to the purchaser.

Without multiple offers, the seller’s position isn’t nearly as strong.

Multi-Offer is Key

When you fail to expose a home to the market, you don’t allow competition to do its job.

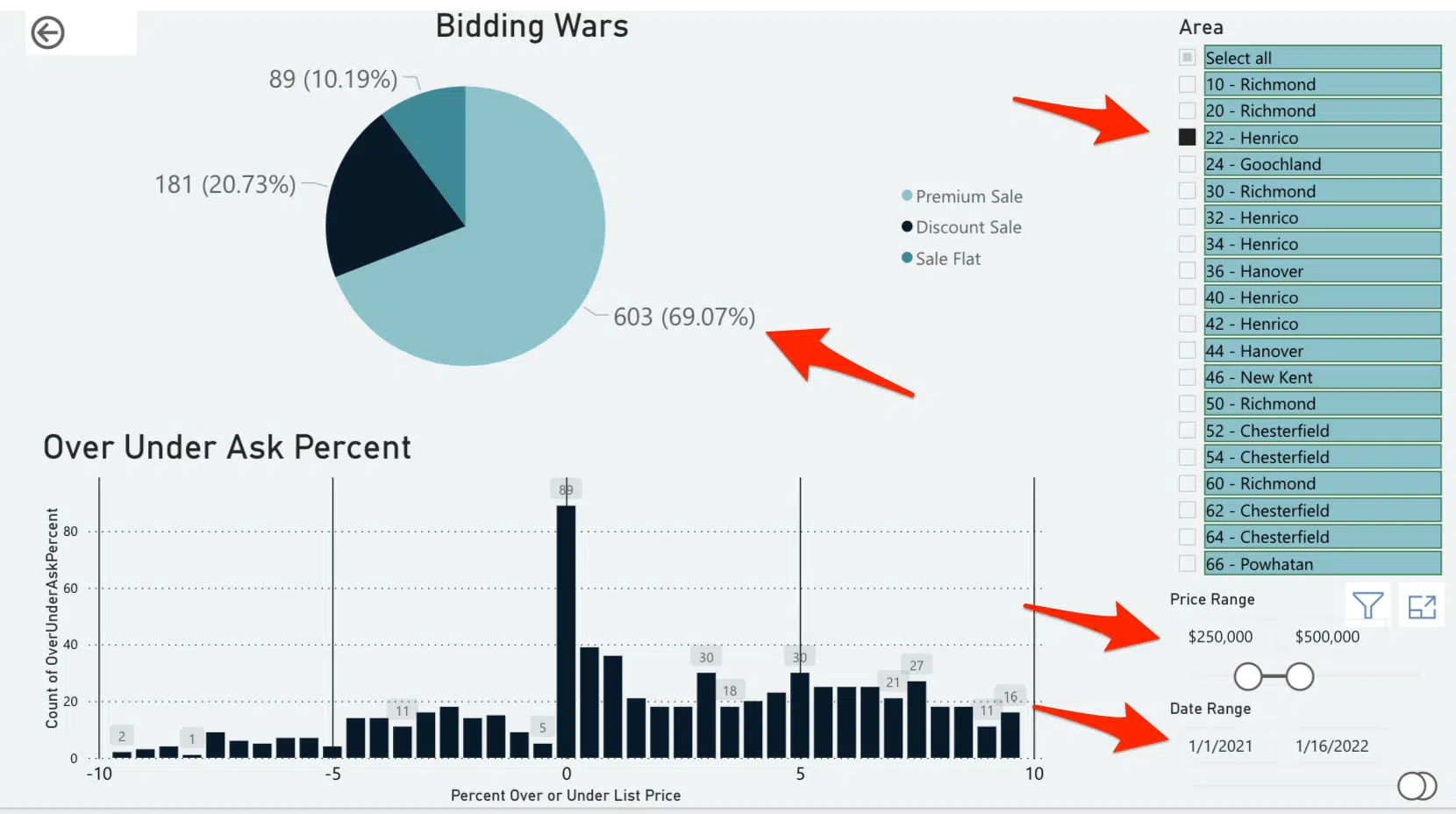

In 2021, nearly 60% of the homes in all of our MLS received multiple offers –– an all time high. But, when you dig deeper and examine specific segments where inventory is especially low and demand is especially high, such as the affordable segment in Richmond’s West End, the number is even higher.

So, when you cut a side deal with a tenant in your rental, or with your neighbor who has always coveted your private back yard, or you accept the unsolicited offer brought to you by an agent with ‘cash buyers from NY,’ you are squandering the leverage an MLS-inspired ‘auction’ creates to not only drive the price higher, but to shift the remainder of the terms well in your favor.

The bottom line is when buyers compete, sellers win.

Summary

I fully acknowledge that sometimes taking an unsolicited offer or off-market sale makes sense, but the cases are far fewer than people would believe. The public just doesn’t understand the power they are giving up when they don’t let the world know that they are willing to sell.

If you get an offer on your home but have not exposed it to MLS, please resist the urge to sell it –– even if you feel the price exceeds your expectation. You are leaving significant value on the table.

Yes, saving some commission dollars may seem like a good idea, but I can guarantee you that the commission you save pales in comparison to the leverage you forfeit by not selling through the MLS in such an inventory-starved environment.

Perhaps in the future, when the market balances itself again, the ability to create a bidding war will subside and the commission you might save could make a back channel sale makes sense.

Today, however, is not that day.