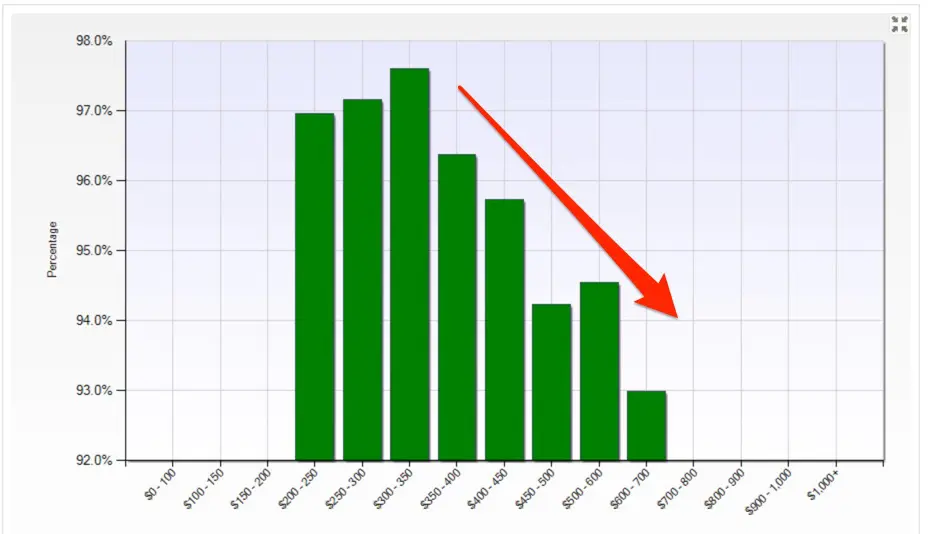

2015 was a really great year for us.

From Humble Beginnings

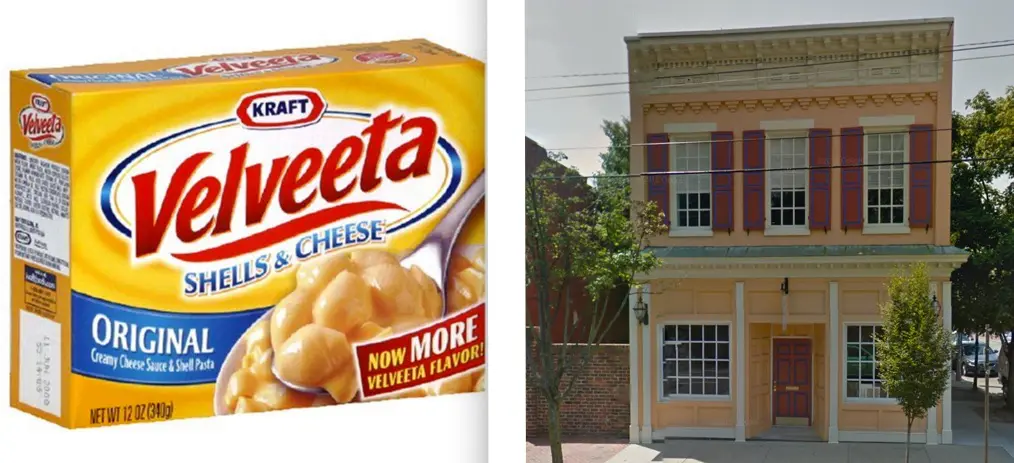

When One South opened our doors in 2008, we were a mere 5 agents, supported by 1 dedicated staff member, in a orange -ish colored building on the edge of VCU (we decided it was the color of Velveeta.) We were nothing more than equal parts blind ambition, blissful naivety and a cool logo.

We Are Growing Up in a Hurry

Fast forward today and we are 60 agents and staff in our new historic office renovation and with a satellite office at the Chesapeake Bay. In the last 2 years alone, we have nearly doubled in both size and volume. Imagine the little marks you make on a door frame to mark you child’s growth … and seeing them double in 24 months! Well, that is pretty much what we did.

But while sales statistics are neat, they are simply the measurement of getting more things right than you get wrong. And several years ago we decided to adopt a stance that I feel has been the main reason we have been not only able to grow, but to grow the right way with a great group of people.

Sharing as a Strategy

About 5 years ago, we made a decision to become a company that shares.

For as long as I could remember, Realtors (and their brokerages) hoarded information. MLS, our own database, was effectively behind a locked door and only the agents held the key. We doled out information, piecemeal, in order to protect our own existence. As long as we governed access, we would be in need, or so said the prevailing wisdom.

But this little invention called the internet changed the game for everyone involved – buyers, sellers AND agents. What we had for years, seen as proprietary information, Trulia and Zillow began to offer completely for free. Needless to say, it has changed the public’s relationship with us and our relationship with them. This disruption forced everyone in our industry to find another way to add value to the process short of acting as taxi service and opening doors. We had to step up our game and really make a difference.

Write It Down

So what did we elect to do? We simply decided to write down everything we knew. We wrote about neighborhoods. We wrote about valuation. We wrote about pitfalls and best practices and we wrote about techniques. We wrote about local issues and we wrote about national ones. We decided that offering what we knew to the public allowed them to research us and see who we were, what we knew and most importantly, how we could help them make a better decision. We made the conscious decision to place our collective knowledge in the public domain for all to see. And you know what, we are glad we did.

You see, having information and knowing what it means are two different things. When you can demonstrate the value you bring to the process through offering your analysis, education and interpretation publicly, people recognize the important role you play. Hoarding information and keeping your analysis to yourself may have worked in 1990 … but it not a winning strategy any more.

2016 and Beyond

Know that as we close out 2015 and head into 2016, we plan on doing more of the same. We will continue to write short bits, philosophical articles and some extremely long exploratory looks at some of the complex topics that require a great deal of effort to break down properly.

Thanks for somehow being connected to One South. We hope to continue to serve you for quite some time.

All industries have jargon … real estate is no different.

All industries have jargon … real estate is no different.